DNY59

High-yielding stocks are very popular on Seeking Alpha.

If you can find a stock that has an >8% dividend yield and write an article about it, it is likely to get a lot of views and comments. On the flip side, if you cover a comparable stock that only offers a 3% yield, you likely won't generate nearly as much interest.

This is probably because there are a lot of retirees on Seeking Alpha, and many of them have not managed to save enough during their careers to earn a comfortable retirement by investing in lower-yielding stocks.

Therefore, they see high-dividend stocks as the solution to their problem.

If you can generate a 10% dividend yield, all it takes is $500,000 to earn >$4,000 each month.

But high yield typically also means high risk, and there are typically good reasons for a stock being priced at such a dividend yield.

I have focused on this segment of the stock market for nearly a decade now and made a lot of mistakes along the way. In today's article, I want to highlight what I wish I had known before I became a high yield investor:

#1 - Growth Shouldn't Be Overlooked Even If You Are A Dividend Investor

You may have heard the quote: "If you are not growing, you are dying." This also applies to high-dividend stocks.

I have seen countless high-yielding stocks turn into disastrous investments because they failed to grow and turned into value traps with their share prices declining just as much, if not more, than the dividend over time, leaving investors with poor returns.

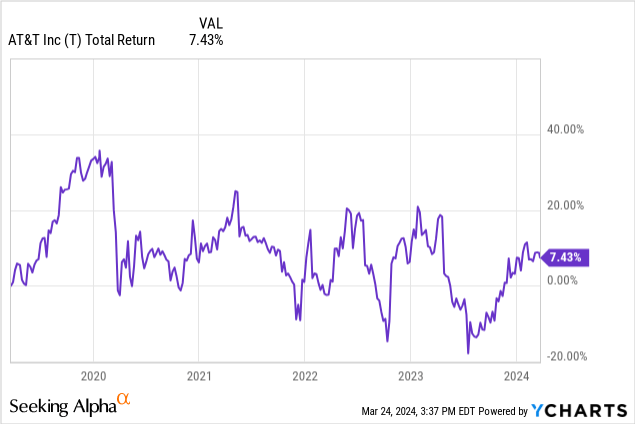

AT&T (T) is a great example of that. Its high dividend yield has attracted a lot of investors, but there is no point in earning a high yield if this comes at the cost of value destruction. The company was paying out too much, failed to grow, and here are the results:

A lot of investors will make the mistake of thinking that if a stock pays them a high yield, then growth doesn't matter. They are satisfied with collecting the dividend and see any additional growth as a mere bonus on top of that.

But the issue is that if a company is failing to grow, all it takes is a little setback and significant value could be destroyed. As an example, if the cash flow is flat, and suddenly interest rates surge, your cash flow will go down significantly. If a new competitor enters the market, there goes some of your market share. If one of your patents runs out, you won't be able to make up for it with other growth avenues.

No business is perfectly steady and consistent, so you need to have some avenues of growth to make up against the occasional setbacks. Otherwise, a high-yield stock will quickly turn into a value trap.

With that in mind, I would much rather earn a growing 7% dividend yield than a flat 9% dividend yield.

#2 - Payout Ratios Can Be Very Misleading

Investors will often think that a dividend is safe simply because its payout ratio is low.

As an example, the dividend yield maybe 9%, but if the payout ratio is just 60%, then it would seem that the company could easily sustain or even grow the dividend.

However, the problem with payout ratios is that they often fail to account for the capex that's required to run the business. This capex may be infrequent but substantial. In that sense, the payout ratio maybe 60% for three years in a row, and it could then surge to 200% in year 4. The average payout ratio over the four years is then dangerously close to 100%.

Moreover, it also does not account for the leverage of the company. A highly leveraged company with a 60% payout ratio could be at much greater risk of cutting its dividend than a conservatively financed company with a 90% payout ratio.

Finally, companies may also lose their ability to access capital over time and this could also cause them to materially reduce their dividend even if the payout ratio is seemingly low.

New York Community Bancorp (NYCB) was still recently offering a high dividend yield for investors and the payout ratio seemed reasonable, but as it began to face troubles, it struggled to access capital and was forced to quickly slash its dividend.

The point here is that the payout ratio can be very misleading and you should not put too much weight on it. It should be just one factor among many others as you assess the sustainability of the dividend.

#3 - Nothing Matters More Than The Alignment Of The Management

Quite often, stocks will be priced at low valuations and high dividend yields simply because the management is conflicted.

From my experience, it is better to stay away from such a situation. No matter how low the valuation gets, a bad management team will always find a way to take from shareholders if that's their goal.

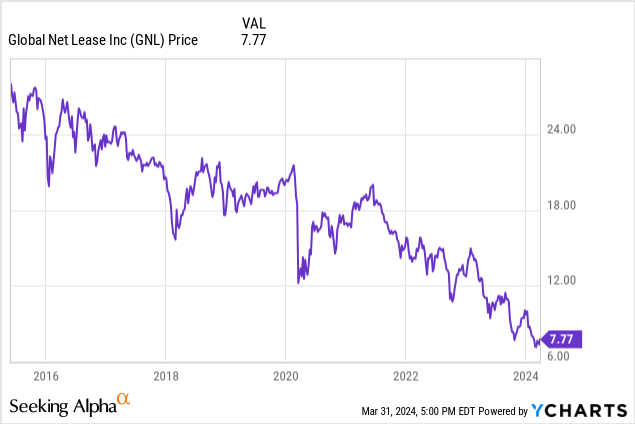

Unfortunately, we see this quite often in asset-heavy sectors like REITs, MLPs, and BDCs. The managers are compensated based on the volume of assets under management and as a result, they will be incentivized to keep issuing more and more shares to buy more assets, even if this comes at the cost of shareholder dilution.

You should avoid such situations at all costs. Earning a 12% yield means nothing if that's matched with a 12% drop in the share price and an eventual dividend cut because the dividend cannot be sustained. I am looking at you, Global Net Lease (GNL):

#4 - High-Yielding CEFs And ETFs Suffer Major Drawbacks

Many retirees will turn to high-yielding closed-end funds, or CEFs, and exchange-traded funds, or ETFs, to earn income, thinking that their diversification and professional management will lower risk and protect them from losses.

But unfortunately, it is often the exact opposite.

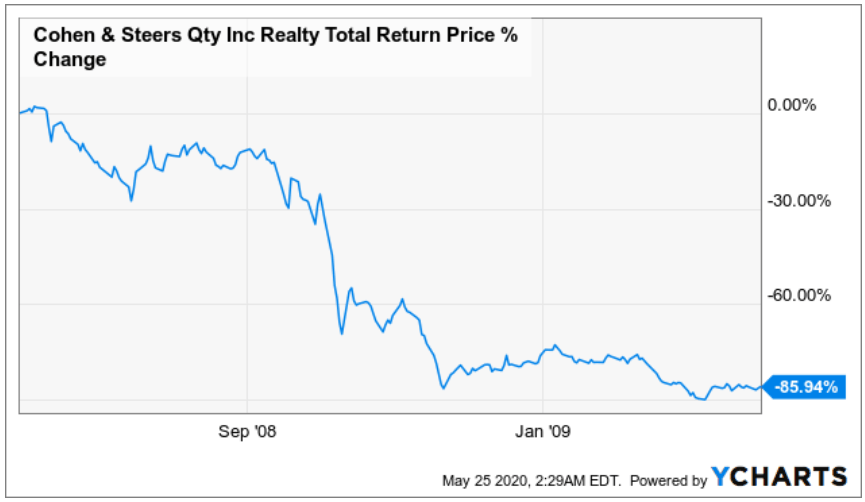

A lot of the most popular CEFs achieve their high yields by taking on additional debt, and their active management is not enough to cover their high fees. In many cases, they will do what we call "window dressing" to avoid deviating too much from their benchmark, and so the vehicle simply ends up being a leveraged high-fee version of the benchmarks. Cohen & Steers Quality Income Realty Fund (RQI) is very popular because it offers an 8% dividend yield, which is a lot more than what its passive benchmarks are offering, but it has only earned 0.3% higher annual returns than unleveraged benchmarks over the long run despite taking far more risk, and almost went bankrupt following the great financial crisis:

YCHARTS

High-yielding ETFs, on the other hand, are not much better because they will often end up owning precisely the type of companies that you should avoid in this segment of the market. A lot of companies are failing to grow or even suffering declining cash flow, and lots of asset-heavy businesses with conflicted management teams.

This is a segment of the market in which you need to be very selective and ETFs generally do a poor job.

#5 - Focus On "Quality Value," Not "Deep Value"

Finally, the biggest and most important piece of advice that I can give you is to not be too greedy.

You shouldn't try to maximize yield. You should instead attempt to optimize the combination of yield, growth, and safety.

That's how you earn good returns in the high-yield space.

Put differently, don't go for the deep value opportunity that offers a 12% dividend yield. In most cases, there are good reasons if the yield is that high.

Instead, go for the 7-8% yielding "quality value" opportunity that's still growing its cash flow, has a good balance sheet, and attractive long-term prospects.

Often, the difference between the two will be that the "deep value" opportunity will be facing secular headwinds, be overleveraged, and/or poorly managed, but the "quality value" opportunity will be discounted just because it is facing a temporary issue that's fixable over time.

I would much rather own a safe and growing 8% yield than a flat and risky 12% yield that's likely to be cut and lead to significant capital losses.

Closing Note

If you want access to our Portfolio that has crushed the market since inception and all our current Top Picks, join us for a 2-week free trial at High Yield Investor.

We are the fastest-growing high yield-seeking investment service on Seeking Alpha with over 1,700 members on board and a perfect 5/5 rating from 166 reviews.

Our members are profiting from our high-yielding strategies, and you won't be charged a penny during the free trial, so you have nothing to lose and everything to gain.

Start Your 2-Week Free Trial Today!