ArisSu/iStock via Getty Images

SoFi Technologies, Inc. (NASDAQ:SOFI) released earnings results for its 1Q24 on Monday morning that beat profit estimates, but also showed a decline in lending activity. Plus, the forecast for the second quarter disappointed, triggering a 10% stock slide.

With that said, however, I think investors overreacted to SoFi’s 1Q24 earnings since the fintech also raised its forecast for all its major metrics (sales, EBITDA and GAAP EPS) for 2024.

I think that SoFi Technologies is a promising turnaround candidate as the company executes on its growth targets and continues to add a boatload of members to its platform, which is where SoFi Technologies’ real magic is playing out.

My Rating History

I reaffirm my Buy stock classification as the fintech is seeing considerable momentum in member and financial services product growth.

SoFi Technologies was just on the brink of achieving GAAP profits last year, which created a promising setup for a re-rating last year (hence my previous Buy rating). The forecast for 2024 implies that SoFi Technologies anticipates to be profitable on both an adjusted EBITDA and net income basis this year.

Considering that the fintech, despite weakness in lending, is seeing robust momentum in members and financial services, I think that SoFi Technologies makes a compelling investment proposition.

SoFi Technologies - Strong Showing For 1Q24

SoFi Technologies beat the average Street profit estimate by $0.01 on Monday and presented a set of financials that was actually quite good.

The fintech raised its forecast for its full-year key metrics (though 2Q24 EBITDA disappointed) and the company saw impressive member growth in its business.

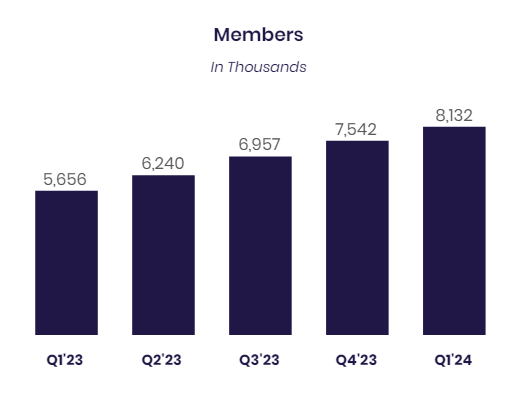

SoFi Technologies’ member count rose 622K QoQ to a new high of 8.1 million. Momentum in member growth is the single biggest reason, in my view, to own SoFi Technologies’ stock as it translates into considerable EBITDA and EPS growth potential down the line.

Members Growth (SoFi Technologies)

SoFi Technologies’ stock dropped more than 10% on Monday, partially because the fintech’s lending segment showed a net revenue contraction, which came as a surprise to investors.

Total lending net revenue fell 2% YoY to $330.5 million, while the segment’s contribution profit also fell. The decline in lending, however, was more than compensated for by SoFi Technologies’ financial services segment.

Lending Segment Results (SoFi Technologies)

SoFi Technologies has built real momentum with its suite of financial services products, which is reflected in substantial growth in this segment. Financial services products contributed $150.6 million in net revenues to SoFi Technologies’ first quarter results, up 86% amid strong demand for such products from the fintech’s members. In total, SoFi Technologies produced $645 million in net revenues in the first quarter, up 37% YoY.

Financial Services Segment Results (SoFi Technologies)

Financial services products are a core component of SoFi Technologies’ growth story, and it is really here where the magic happens. SoFi Technologies had 10.1 million financial services products on offers at the end of 1Q24, reflecting a YoY growth rate of 42%. Lending products, on the other hand, only saw 20% YoY growth.

Products By Segment (SoFi Technologies)

Investors Likely Overreact To 2Q24 Forecast

SoFi Technologies presented a robust forecast for 2024, but 2Q24 sales projections fell short of Street estimates, further explaining yesterday’s 10% price correction to the downside.

SoFi Technologies forecast $555-565 million in adjusted net revenue for 2Q24, which came in below the Street’s average estimate of $581 million.

Adjusted Net Revenue Forecast (SoFi Technologies)

With that said, however, SoFi Technologies did hike its full-year net sales outlook (to $2,390-2,430 million), its adjusted EBITDA outlook (to $590-600 million) and its GAAP projection (to $0.08-0.09 per share). All three metric increases underpin the investment thesis for SoFi Technologies and help paint an overall healthy picture of the fintech’s growth.

GAAP Net Income Guidance (SoFi Technologies)

Low Sales Multiple For The Associated Upside

SoFi Technologies forecast $0.08-0.09 per share in GAAP profits in 2024 which matches the consensus Street forecast. SoFi Technologies only just became profitable, so some investors may not like that I am using an earnings multiple to value the fintech, but given the rapid anticipated growth in EPS, I think a P/E ratio can be used for SOFI.

The market models a three-fold increase in GAAP profits in 2025, YoY, which is a reflection of the fintech growing its member accounts aggressively while scaling its non-lending product offers.

Earnings Estimate (Yahoo Finance)

Based on next year’s earnings, SoFi Technologies is selling for a very sensible 30x earnings multiple and the fintech can be expected to deliver double-digit (if not triple digit) profit growth annually in the next one or two years.

PayPal Holdings Inc. (PYPL) is selling for 12x leading (2025) earnings, but the fintech is growing much more slowly than SoFi Technologies and is struggling to keep customers on its platform, while SoFi Technologies is absolutely crushing it right now in terms of account growth.

I think that SoFi Technologies could double its profits YoY in 2026, to $0.50 per share, and with an earnings multiple of 30x, the fintech could re-rate to $15, which is where I see SoFi Technologies’ intrinsic value. This implies an approximate doubling in the company’s stock price, and I believe that this valuation would more accurately reflect SoFi Technologies’ impressive growth results in 1Q24.

Why The Investment Thesis Might Not Pan Out

The market has been hesitant as of late to reward SoFi Technologies for the considerable progress the fintech has made in the recent past.

Firstly, the student loan payment freeze was reversed last year and SoFi Technologies achieved GAAP profitability in 2023 as well, a milestone event by any means. At the same time, SoFi Technologies’ growth has been underpinned consistently by substantial net increases in the member base.

Considering these factors, I think that the risks for SoFi Technologies are rather limited, though investors that focus primarily on the fintech’s lending activity did have a point in pointing out that SOFI is seeing softening momentum in this particular segment in 1Q24.

My Conclusion

I think the market has lost its mind when it comes to SoFi Technologies.

The fintech may have seen a tiny downturn in lending-associated net revenues, but the real growth for the company is not in lending, it is in financial service products. This makes the market’s response to the company’s 1Q24 earnings even more irrational.

I believe that SoFi Technologies is a very well-managed fintech company and the increased growth forecast for earnings, EBITDA and sales is underpinning the core growth investment thesis.

The risk/reward relationship is quite favorable on the drop, in my view, and I think that SoFi Technologies could be a very solid, long-term investment for investors that focus on the intact, underlying member growth story.